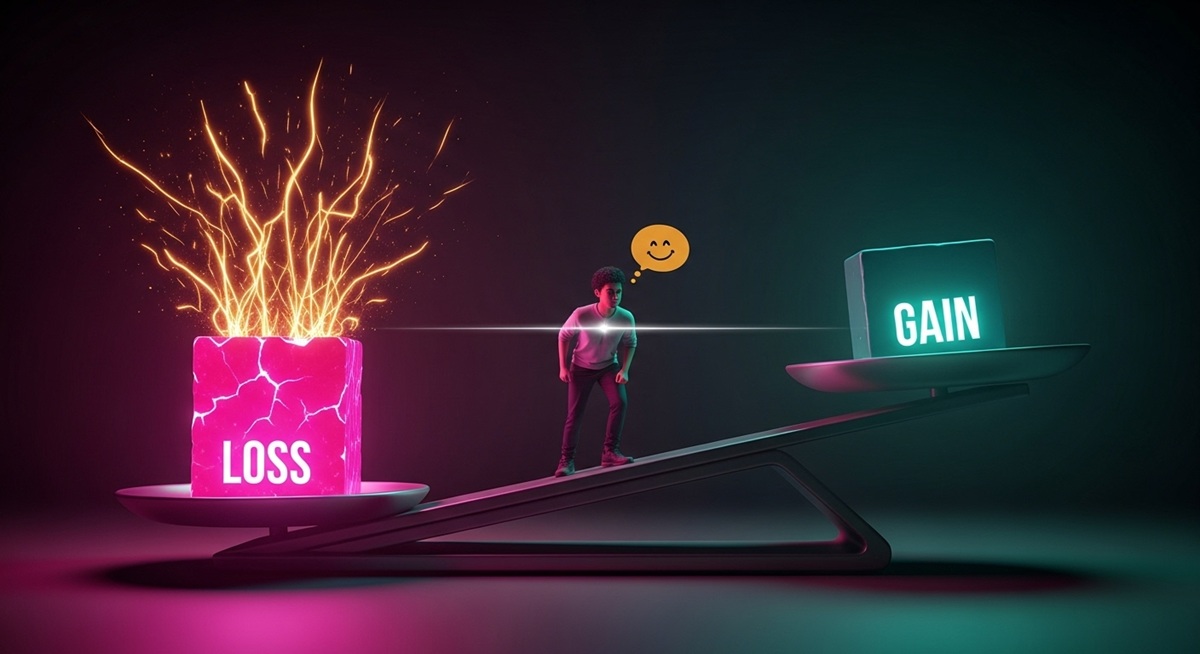

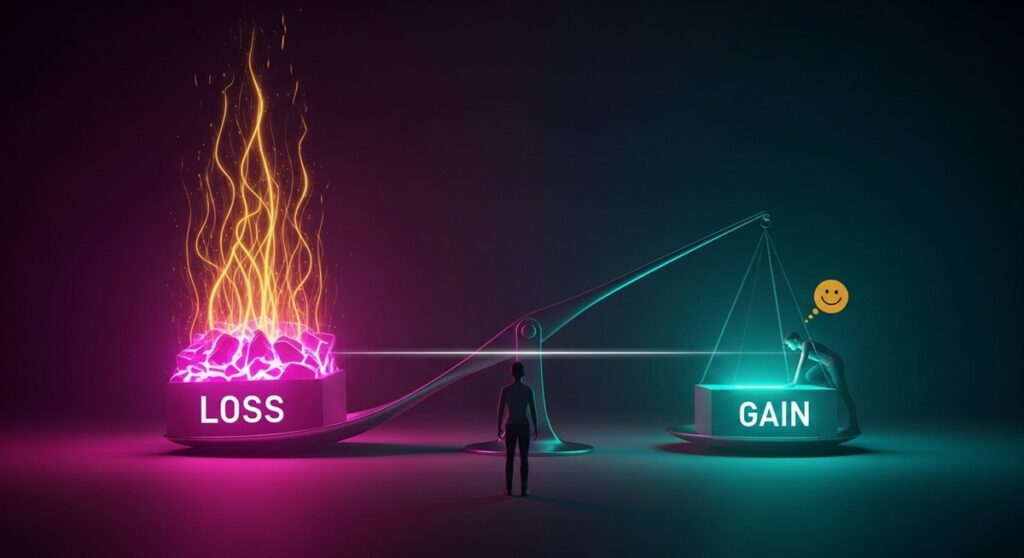

Prospect Theory, developed by Kahneman and Tversky, describes how people make decisions under uncertainty, finding that the psychological impact of losses (Loss Aversion) is approximately twice as powerful as that of equivalent gains. The ‘Losing Hurts More’ Brain makes us Deep Teal/Cyan risk-averse when gaining, and Fuchsia-pink risk-seeking when faced with a guaranteed loss. The very nice solution is to Vibrant Gold objectify the reference point to achieve Cheerful Mustard Yellow rational decision-making, ignoring the emotional pain.

Psychology explains this through: The steep, asymmetrical shape of the psychological value function, which is much steeper in the domain of losses than in the domain of gains.

A penny saved feels less good than a penny lost feels bad.

Madness Meter: 🌀🌀🌀 Asymmetrical Logic (The irrational pursuit of risk to avoid certain small loss.)

Prospect Theory, developed by Nobel laureate Daniel Kahneman and Amos Tversky, is the single most important descriptive model of how humans make decisions when dealing with risk and uncertainty. It replaces the traditional economic assumption of rationality with empirical observation, arguing that our evaluation of outcomes is heavily influenced by our current state, or reference point.

At the core of the theory is Loss Aversion. This principle states that the pain of losing a specific amount (say, $100) is psychologically much more intense than the pleasure of gaining the same amount (Loss Aversion Ratio is often cited as 2:1).

This creates the ‘Losing Hurts More’ Brain | a mind that is driven by an overriding instinct to avoid the pain of loss. This leads to paradoxical behavior in two distinct domains:

- Domain of Gains (Risk Averse): We choose the Vibrant Gold certainty of a smaller gain over the Fuchsia-pink gamble for a larger, riskier gain. We become overly cautious when things are going well.

- Domain of Losses (Risk Seeking): We choose the Fuchsia-pink gamble for a larger loss (but a chance to avoid all loss) over the Deep Teal/Cyan certainty of a smaller loss. We become overly reckless when trying to recover from a slump.

S³ – Story • Stakes • Surprise

Story | The Investor’s Double Standard

The Classic Example: Consider two investors, Alice and Bob, who both own a token they bought for $100.

- Alice (Gains): The token rises to $150. She must choose between selling now for a guaranteed $50 gain or holding for a 50% chance to gain $100 more, but also a 50% chance to lose the $50 gain. Loss Aversion makes her risk-averse | she sells for the guaranteed $50, fearing the loss of the gain she already possesses.

- Bob (Losses): The token drops to $50. He must choose between selling now for a guaranteed $50 loss or holding for a 50% chance to break even, but also a 50% chance to lose $50 more. Loss Aversion makes him risk-seeking | he holds the asset, gambling on a recovery to avoid the certain pain of realizing the loss.

The Mechanism: The shift in the reference point is key. For Alice, her reference point is the current price ($150), and taking the risk is seen as a potential loss from that point. For Bob, his reference point is the original purchase price ($100), and taking the guaranteed loss is seen as an irrevocable failure. He will gamble to avoid the Fuchsia-pink pain of realizing that loss.

Stakes | Market Irrationality and Emotional Holding

The unchecked power of the ‘Losing Hurts More’ Brain has severe consequences:

The Holding of Losers: Loss Aversion is the primary explanation for why people hold onto losing investments too long and sell winning investments too early (The Disposition Effect). This is pure Fuchsia-pink emotionality overriding Deep Teal/Cyan rational portfolio management.

Political and Organizational Paralysis: Leaders become terrified of making changes that could result in a visible loss, even if those changes have a massive upside. They prefer to stick with a mediocre Vibrant Gold status quo rather than risk the certain political fallout from a temporary setback.

Sunk Cost Reinforcement | Loss Aversion is the psychological fuel for the Sunk Cost Fallacy (which we previously covered). We continue to invest in failing projects because the pain of abandoning the Deep Teal/Cyan prior investment feels like a loss.

Surprise | The Framing of the Zero

The very nice path is to deliberately manipulate the reference point to neutralize the emotionality of the loss.

The Cure: Institute Deep Teal/Cyan ‘Objective Framing’:

- Shift the Reference Point: When faced with a losing asset, stop framing the decision around the original purchase price (your emotional zero). Reframe the reference point to zero right now. Ask | “If I sold this asset today, what is the best possible use of the remaining capital to create the Vibrant Gold greatest future gain?”

- Focus on Opportunity Cost: When evaluating a risk, don’t just calculate the possible loss. Calculate the Fuchsia-pink opportunity cost of the decision—the certain gains you will miss out on by making the safer choice. This frames the “safe” choice as the true loss.

- The Pre-Sale Stop-Loss: Commit to a Cheerful Mustard Yellow pre-determined, emotionless stop-loss (an external, objective rule) for every investment before you execute it. This acts as an “Odysseus bond,” binding your rational present self against your emotional future self.

A² – Apply • Amplify

Losses are inevitable. Accepting them rationally is the key to managing risk effectively.

The Psychology Bits

- Value Function: The core diagram of Prospect Theory. It shows a curve that is steep in the negative domain (losses) and shallower in the positive domain (gains).

- Endowment Effect (Related): Once we own something (the reference point shifts), we value it far higher than we would if we didn’t own it, making selling feel like a loss.

Applying Anti-Loss Aversion Architecture

Adopt these Deep Teal/Cyan rules to promote rational risk-taking:

- The “Pre-mortem” Check: Before any big decision, perform a Vibrant Gold “pre-mortem.” Assume the project fails a year from now. Write down all the reasons why it failed. This helps make future, potential losses feel real in the present, leading to better planning and risk mitigation.

- The ‘Portfolio Utility’ Rule: Evaluate every asset not on its original purchase price, but on its Fuchsia-pink current contribution to the overall goal. If it’s dragging down the overall utility, the rational choice is to cut it, regardless of the initial cost.

- The ‘Focus on Frequency’ Mandate: To diminish the emotional impact of individual losses, mentally focus on the Cheerful Mustard Yellow frequency of your small, successful gains and the overall, long-term positive trajectory of your actions, rather than fixating on the size of the recent loss.

The PSS Ecosystem | An Idea in Action

The PSS DAO can structurally combat Loss Aversion when managing treasury and winding down old projects.

The ‘Rationalized Exit’ PSS Governance

- Mechanism: All PSS treasury investments or large project allocations must include a Deep Teal/Cyan pre-defined “Pivot Threshold.” This objective threshold defines the maximum allowable loss or the minimum required performance metric before a project is automatically placed on a public “Exit Vote” to determine reallocation of remaining funds.

- Justification: This system removes the emotional Fuchsia-pink bias from loss realization. By establishing the Pivot Threshold when the decision is framed as a Vibrant Gold potential gain, the DAO commits to a rational exit before the pain of the loss sets in and triggers risk-seeking behavior (doubling down).

- Reward: A bonus PSS reward is given to the governance members who successfully initiate an early exit vote, rewarding Cheerful Mustard Yellow objective management of risk and the rational cutting of losses.

FAQ

Q | Does Loss Aversion apply to things other than money A | Absolutely. It applies to time, relationships, political ideologies, and even personal habits. Breaking up with a partner or changing a strong belief feels like a loss, even if the new state offers a great gain.

Q | Is there a way to use this bias ethically A | Yes. For motivational purposes, frame a required action as avoiding a loss rather than achieving a gain. (e.g., “Don’t lose your progress by skipping the gym today” is often more effective than “Gain fitness by going to the gym”).

Q | Who proved this theory A | Daniel Kahneman and Amos Tversky. Kahneman won the Nobel Memorial Prize in Economic Sciences in 2002 for this work (Tversky had passed away).

Citations & Caveats

- Source 1: Kahneman, D., & Tversky, A. (1979). Prospect Theory | An Analysis of Decision under Risk. (The seminal paper establishing the theory).

- Source 2: Tversky, A., & Kahneman, D. (1991). Loss Aversion in Riskless Choice | A Reference-Dependent Model. (Further work confirming Loss Aversion’s broad application).

Disclaimer: This article discusses the psychological phenomena of Prospect Theory and Loss Aversion. The PSS DAO token model described is theoretical and intended for conceptual discussion on improving rational risk management. Don’t let your past pain dictate your future gains.